Should life insurers benefit from dodgy advertising under fictitious names?

With the potential for a ban on lead generation for financial services, the life insurance industry body, the Council of Australian Life Insurers (CALI) argues for life insurers to be exempted. (see IFA News 10/6/26). Admittedly, the risks for consumers are not as great as they are for superannuation and investments, and there is arguably a place for allowing life insurers to receive consumer enquiries through legitimate comparison sites. However, that is not the only example of lead gen for life insurance.

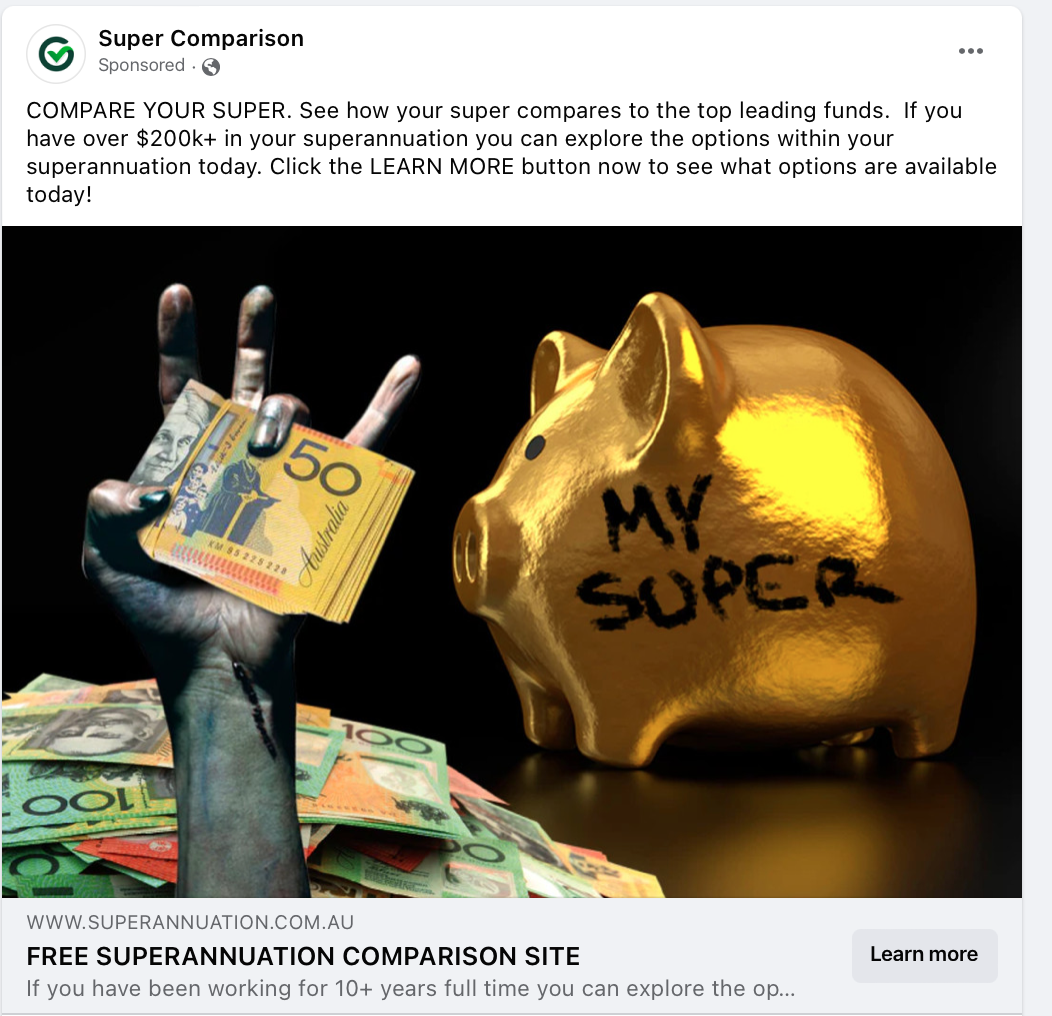

The Australian Government is considering how to curb lead generation activity, following over one billion dollars in losses by consumers who were funnelled to unethical advice via lead generation advertising. So what happens if you respond to a “free superannuation review”?

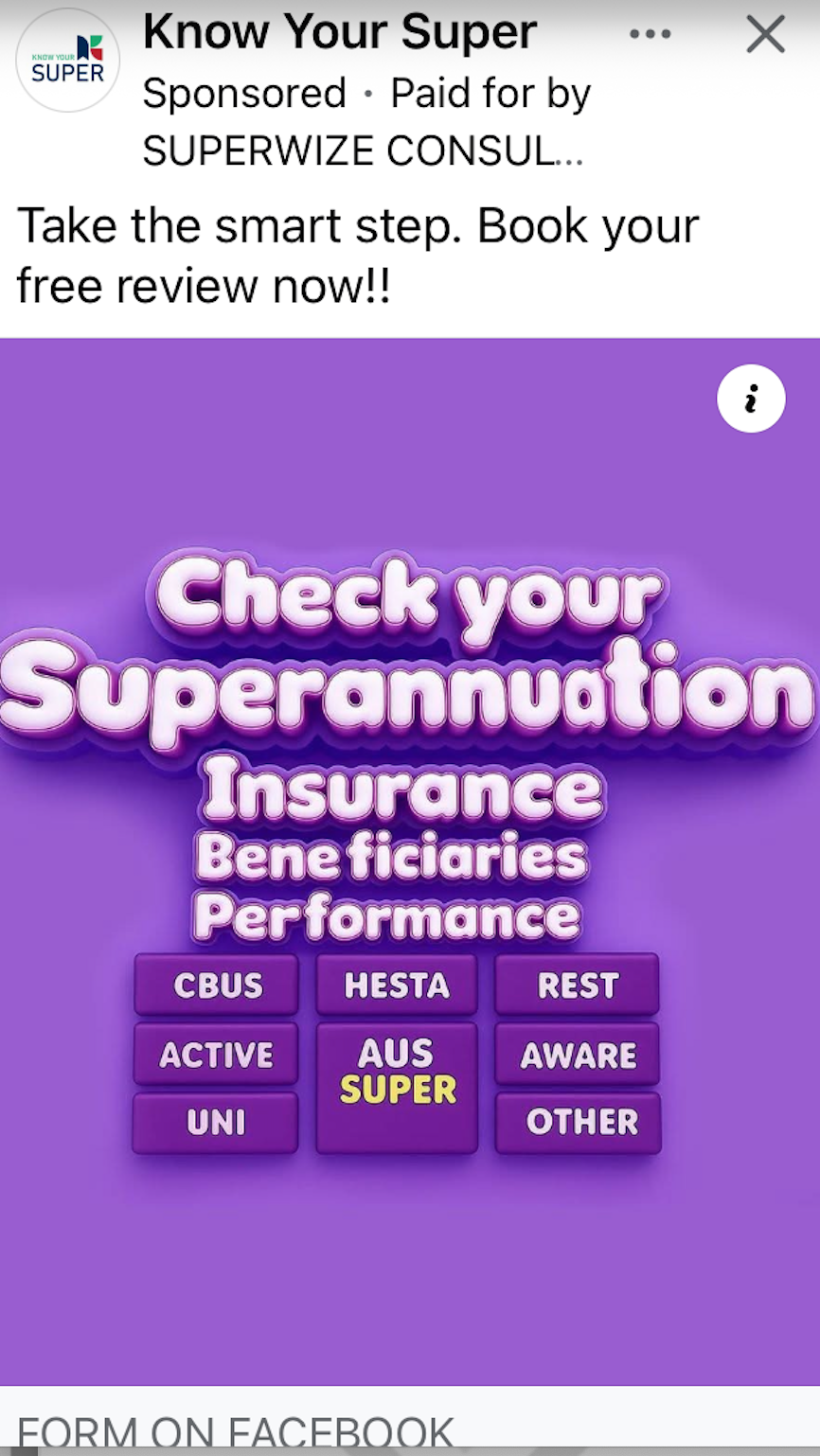

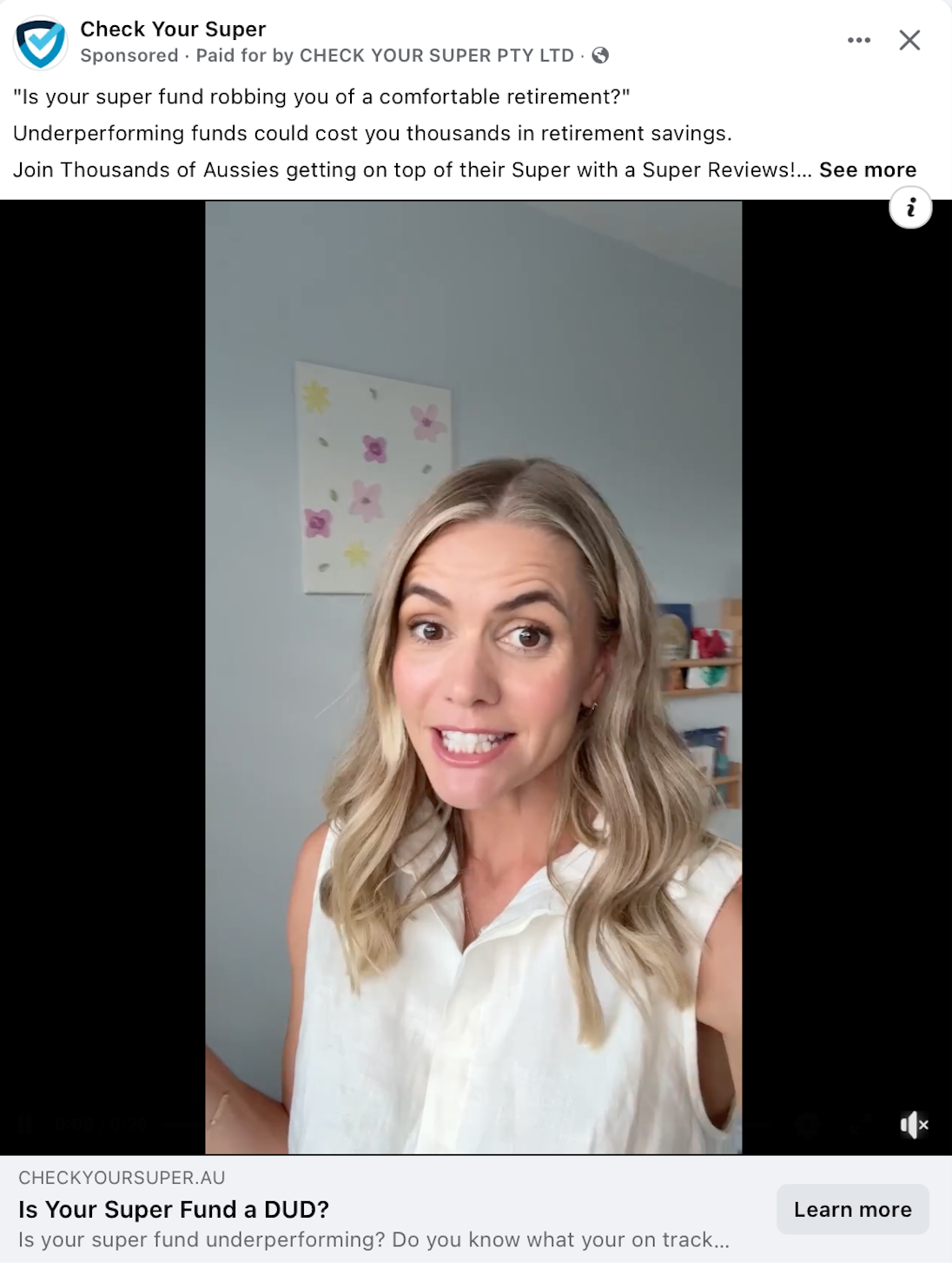

Social media is still full of these lead generation ads, so it’s not difficult to find out.

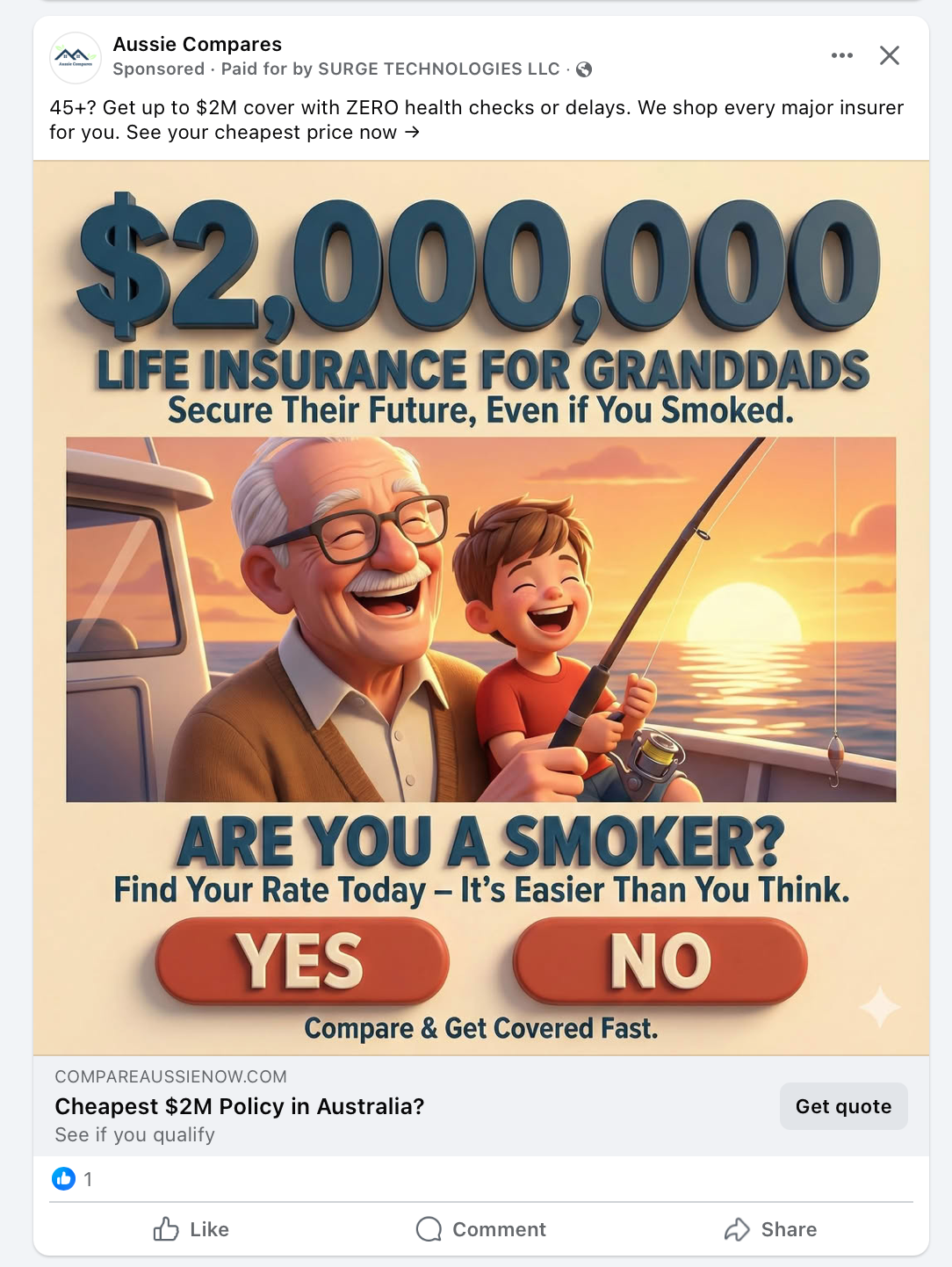

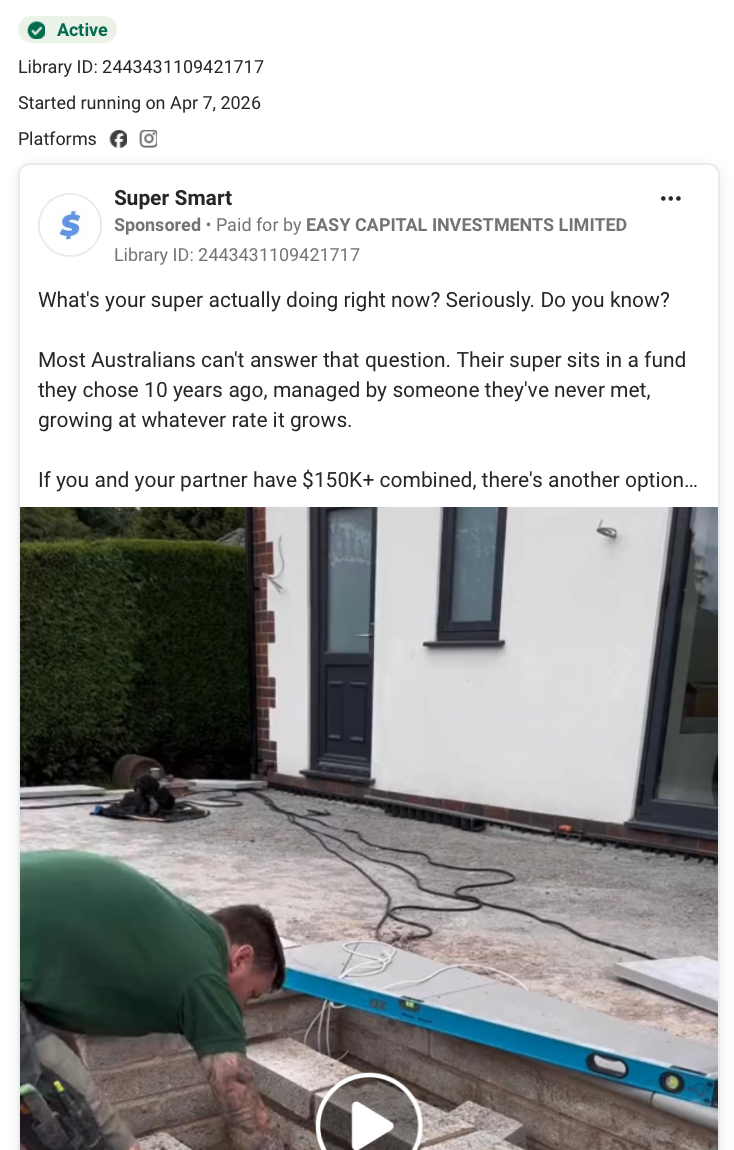

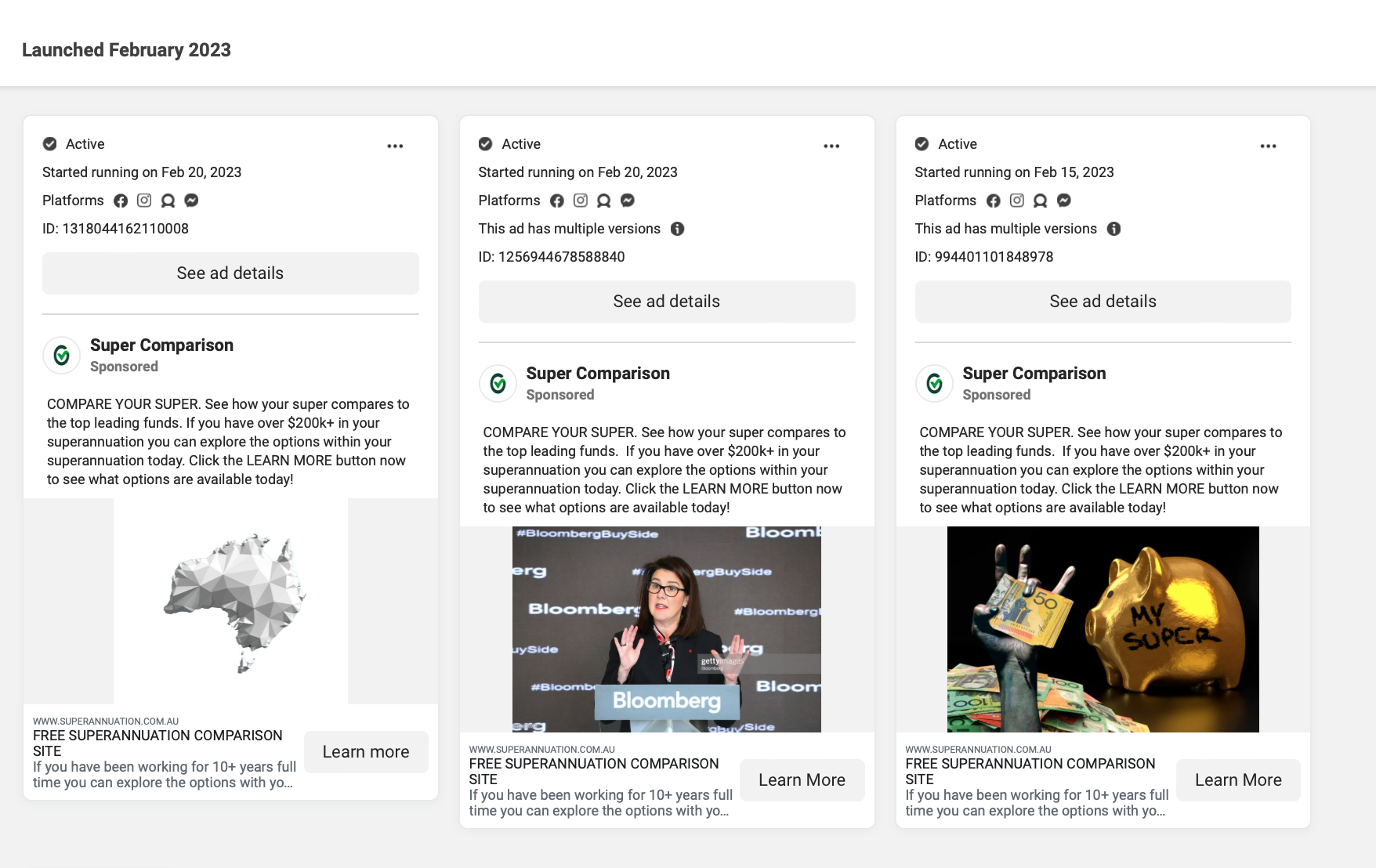

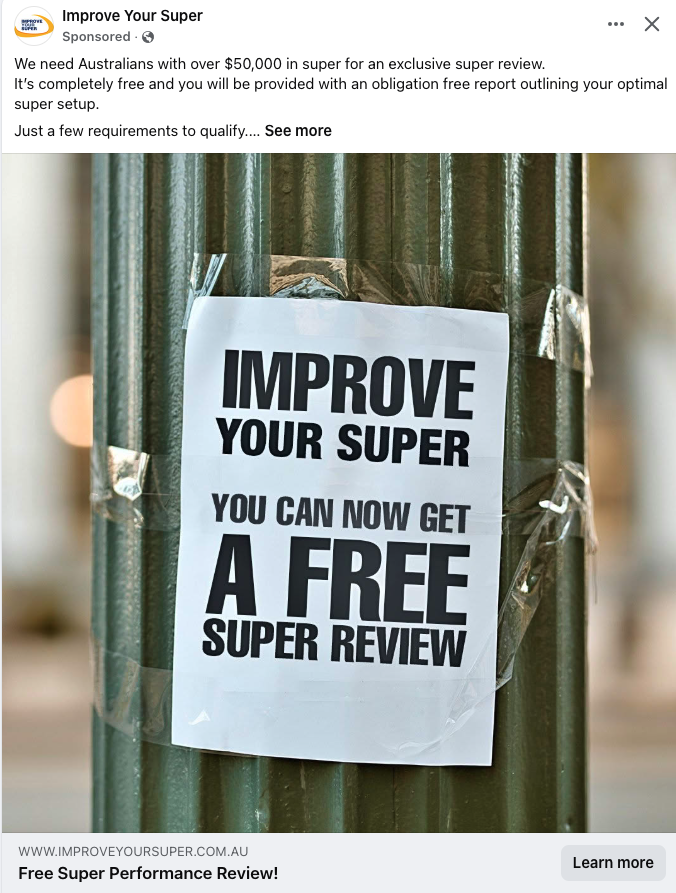

This week I responded to a Facebook ad by “Super Smart”. The video said “review your super performance in just 60 seconds …. just click the link below it’s free.” Other ads by Super Smart promoted property investing through superannuation. These ads suggested there was some urgency, claiming that the law that allows this could change soon.

The ad identified that it is paid for by NZ company Easy Capital Investments. It appears that the director of Easy Capital Investments is also a director of Velocity Leads.

Within minutes I received a text referring to my enquiry, saying to expect contact from Advisor Link.

I received a phone call 5 minutes later from Advisor Link (I think all communication was with Travis Seckold, the director) asking for some information so my free report could be prepared.

The office in Queensland where Next Generation Wealth operated. Lead generation firms have also operated from this address in the past – and one is based there currently.

For these consumers, the journey to disaster often started with an innocent looking ad, offering to “compare super funds”.

It’s unrealistic to expect lead generation firms, which are in the business of marketing, to vet the quality and ethics of a licensed financial service – so the fault lies with the licensed financial businesses – and AFSL licensees should be banned from taking these leads.

The ads rarely name a real business – either of a licensed financial service or even the lead generation business that posts the ad. The same lead generation firm might advertise using more than one fictitious name.

These types of ads are still prolific on social media in 2026.

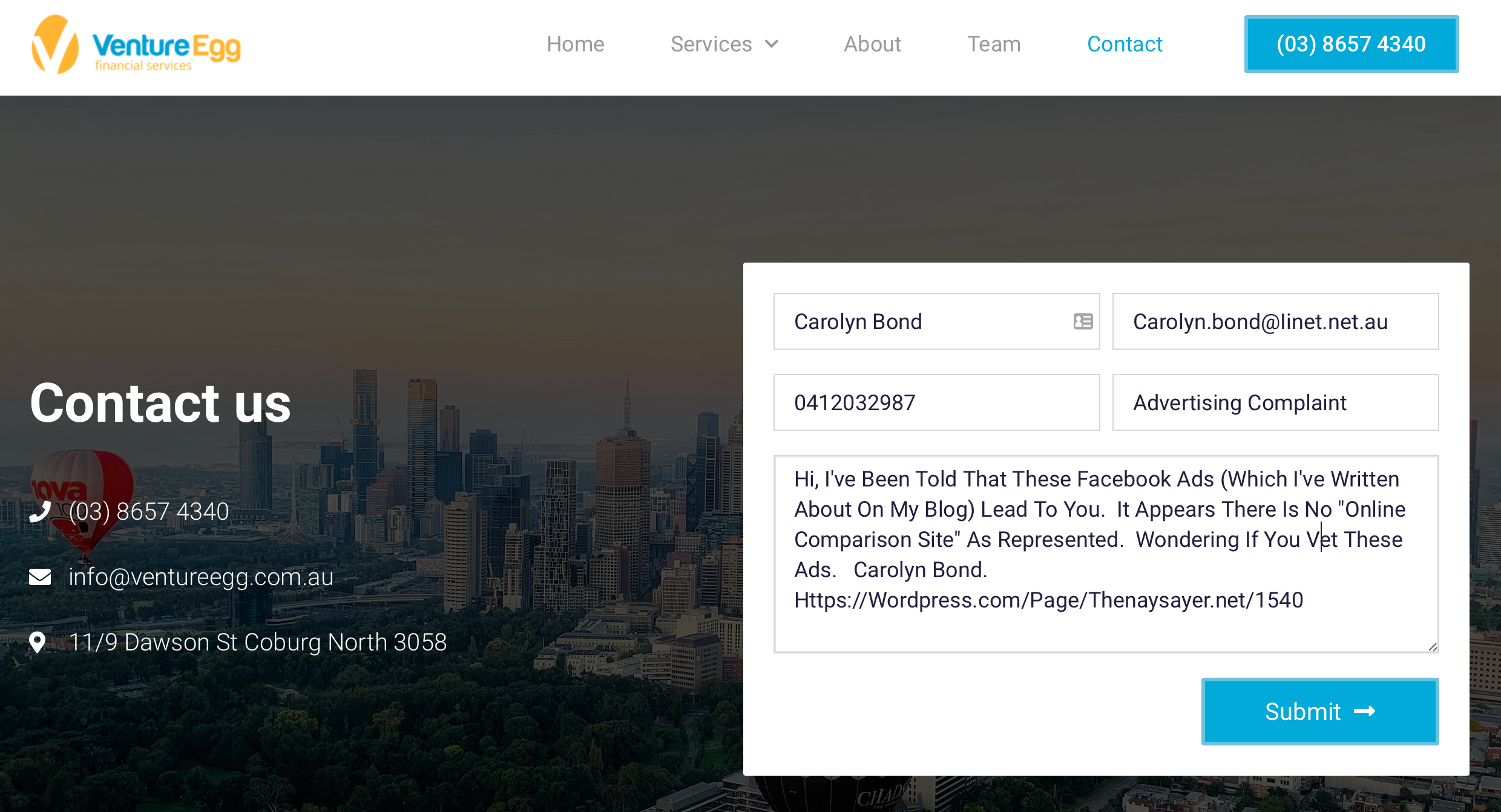

Here are just some of lead generation ads from 2023. Some resulted in calls to me from Next Generation Wealth or Venture Egg, or another business related to this scandal.

Lead generation ads for financial services either result in legitimate businesses obtaining customers through misleading ads (probably in breach of anti-hawking provisions1) or they lead to scams.

My recent experience shows the role lead generation plays in scams, and how difficult it is to identify a scam.

I responded to this ad by “Rate Grid” on Facebook on 18th January.

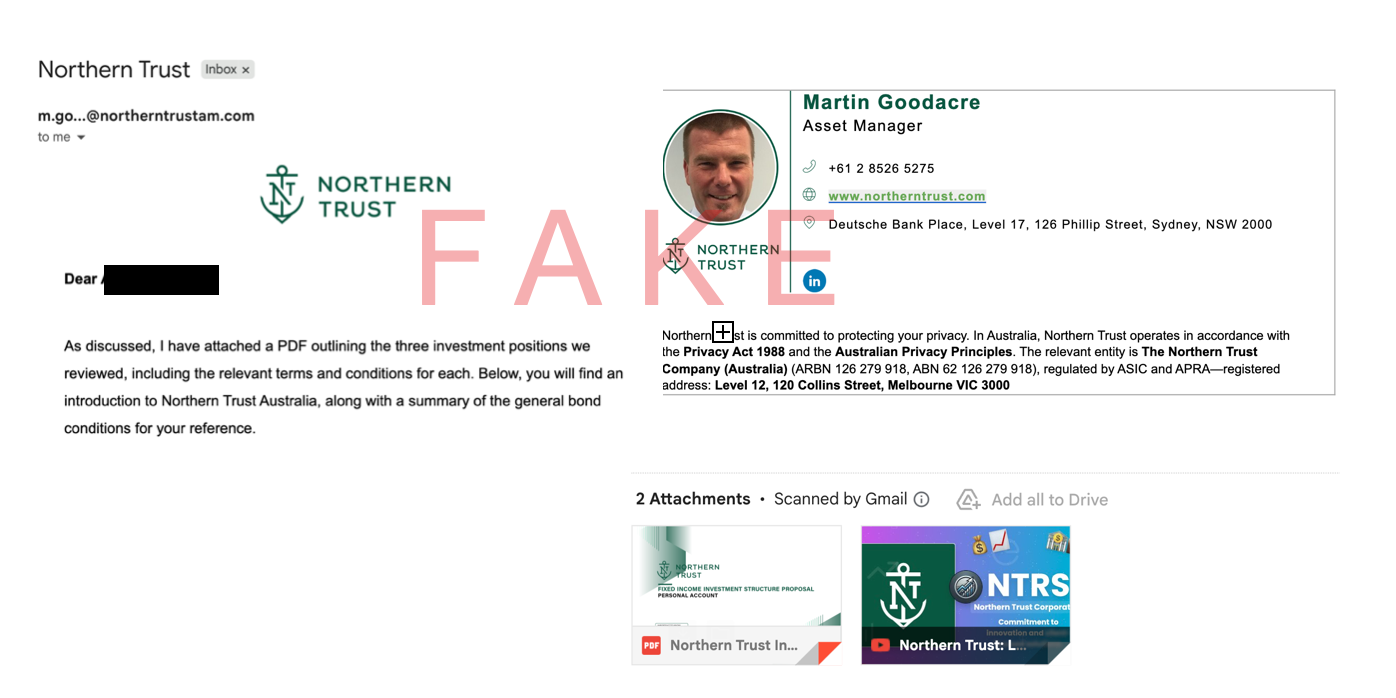

Two days later, I received a phone call from someone who identified themselves and named a large, investment firm. I’m not naming the firm in the text here because I believe the firm wasn’t involved.

I was asked if I was interested in investing in bonds, and after a brief discussion the caller agreed to email details to me. The email contained information about investing in bonds, and (wrongly) stated that the investment would be protected by the Financial Claims Scheme in Australia. See below for some excerpts.

The email looked legitimate. The sender’s name was the same as an employee of the legitimate company (including a photo). All links in the email went to the website of the legitimate company which holds an AFSL.

However, the domain on the email address was slightly different to the company’s website. The additional “AM” in the domain (see below) could make sense, as the company’s name ended in “Asset Management” (although they didn’t use that, or “AM” in their web address). I typed in the website using the domain in the email – and it redirected me straight to the legitimate company’s website.

While a redirect could be legitimate, for example if a business had changed its URL at some point, a check of the domain name showed that the domain name (with the additional “am”) had only been registered a few weeks ago.

These lead generation portals are being used by both licensed businesses and scammers, leading to various levels of consumer detriment. There are no simple solutions to scams, which must be attacked on many fronts. However, one positive step would be for ASIC to ban all AFSL holders from receiving individuals’ details through lead generation.

This is likely to breach the anti-hawking provisions because the consumer is induced to consent to the contact so that the consumer can take up a product/service that is different to that offered by the advertisement). See ASIC’s RG 38.68. ↩︎

Lead generation ads on Facebook for financial services can link to scams, or ‘click bait’ promising unrealistic returns that can lead people to switch to risky investments.

Lead generation ads are placed in a bogus business name, often without disclosing the company providing the services, so it’s not possible to know which licensed financial service (if any) is benefiting from the ads.

While it won’t solve all the problems, it is positive that Meta (Facebook) has signed on to the Australian Online Scams Code, and has developed a new process for financial services advertising in line with the Code’s commitment to “Deploy measures to protect people from scam advertising.”

So you can still lose money, but at least you’ll know who’s responsible!

Rates Compare and Capital Guard

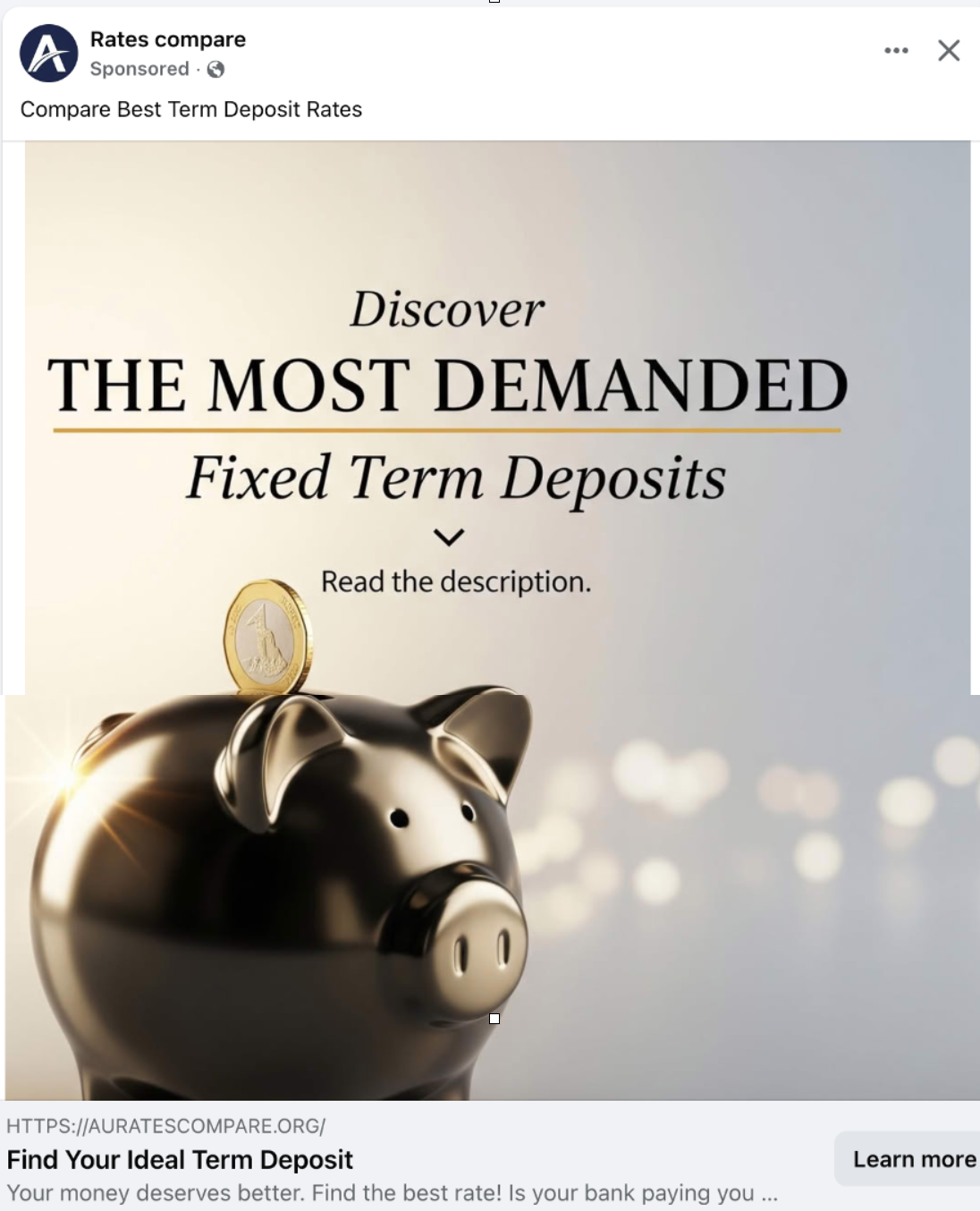

While most of the financial services ads I see on Facebook now identify the advertiser, there are exceptions. Like this one, which advertises “term deposits’. The advertiser ‘Rates Compare’ isn’t a real company, and the name of the owner of the website is hidden. My response resulted in a phone call from Capital Guard which holds an AFSL.

A decision to ban Dominique Grubisa from practising law found, among other things that Grubisa:

instructed private investigators to pretend to be her customers to mislead, and get privileged information, from another solicitor

allowed two banned lawyers (her parents) to work for her legal practice in breach of the law

made misleading and deceptive representations in relation to an asset protection scheme – the Master Wealth Control (MWC) asset protection product (her so-called “Vestey Trust”)

failed to provide competent legal advice

acted where there was a conflict of interest by acting for her own company (MWC) as well as for customers of MWC; and

instructed her solicitors to provide misleading information to the Council of the NSW Law Society which was investigating this case.

On 1 October 2025, the NSW Civil and Administrative Tribunal (Occupational Division) recommended that Dominique Grubisa be removed from the Roll of Solicitors maintained by the Supreme Court of NSW. This means that, like her parents, she will be prohibited from practising law for life.

NCAT found that her conduct represented:

“very serious and persistent departures from a reasonable standard of competence and diligence. That conduct included incompetent legal advice, misleading the Law Society, arranging and approving of investigators attempting to obtain privileged information from another solicitor by deception and failing to appreciate and act on clear potential conflicts of interest, amongst other things.

Compounding this conduct is the Respondent’s apparent inability to appreciate the seriousness of her conduct which, as the Council submitted gives the Tribunal no confidence that she would, if she were to remain practising, not act in the same way.”

This decision adds to Grubisa’s woes including $1 million fine from the Federal Court for misleading consumers, being banned as a company director by ASIC, becoming bankrupt and receiving a ‘smack down’ from the “Privacy Commissioner” for misusing property data.

Regulators have recently warned the public about lead generation advertising,. ASIC says that “superannuation checks” are used as a back door into the high-pressure telemarketing and have led to financial advisers putting clients into inappropriate financial products – naming entities First Guardian Master Fund, Shield Master Fund, Venture Egg and Financial Services Group.

While responding to these ads won’t cause everyone to lose retirement savings, why take the risk of sharing personal financial information, and inviting contact from someone you don’t know?

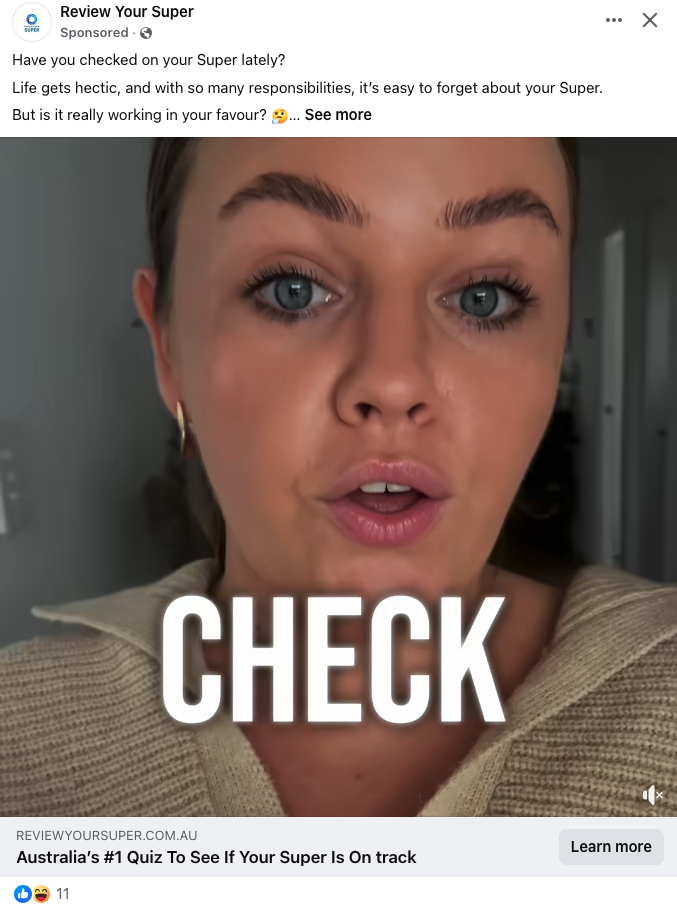

I wrote previously about lead generation, but this week I had another look. Once I started searching the web and Facebook to compare superannuation products, the Facebook ads started popping up. Here is a small selection of the ads on my Facebook in the last 48 hours.

Well, it’s the end of the road as far as her defence against the ACCC’s action against her for misleading and deceptive conduct. Yesterday, the High Court rejected her application for an extension of time to lodge an appeal against the Federal Court’s decision.

See here for details of this case and links to the court decisions.

Meanwhile, after a raft of regulatory action against her (including by the Law Society, Privacy Commissioner, ASIC and the ACCC) Grubisa continues to be philosophical about things!

Her regular posting on FB and Instagram include renovation and property tips, as well as inspirational (mis)quotes & affirmations.

Her facebook page info links to propertylovers.com.au – a business owned by her husband.

And this final quote (or misquote) she shares, suggests that all the criticism and legal challenges she has faced, are just further steps on her way to success!!

Update 2026: Council Watch’s activity appears to have been limited following media reports of accusations against its head Dean Hurlston of stalking and harassing a mayor, apologising to a deputy mayor he accused of sexual harassment and reports of more than 20 councillors accusing the group of abusing councillors and spreading misinformation.

Council Watch Victoria claims to represent ratepayers – but are its views shared by most Australians?

Independent research[i] reveals that “Australians increasingly have an appetite for local government to address contentious cultural and political issues”.

However, Council Watch argue otherwise based on biased surveys, and encourage angry comments on their Facebook page about issues such as flying inclusive flags, Welcome to Country and changing the date of Australia Day.

Dominique Grubisa suggests that her parents suffered at the hands of a bank – but is it true?

Far from being ‘innocent’ consumers ripped off by a bank, both were lawyers who incurred large debt due to her father’s gambling ($14 million over 5 years was reported) and misappropriating clients’ trust money. They still owed the bank $1.5 million after their three properties were sold.

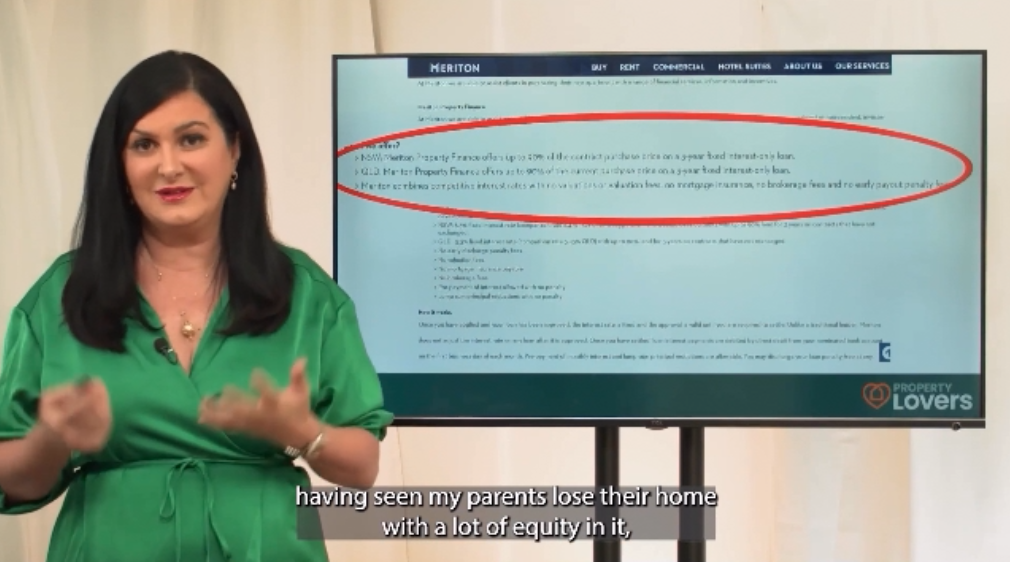

Grubisa currently claims in one of her videos “I’ve seen my parents lose their home with a lot of equity in it, no word from the bank, no accounting of what was left over and no change given”.

She shares this, and similar anecdotes, to support her message that when banks repossess a home “equity in a property is fast eaten up in fees and charges banks”. This is a toned-down version, since her claim that “banks don’t give change” was found by a court to be misleading.

So, what really happened to her parents?

Court records show that after the sale of three properties, Christoper Fitzsimons and his wife Maria still owed $1.5 million to the bank – debt they owed, in part, due to Christopher’s gambling and misappropriation of trust money.

Grubisa’s parents fought legal action for 8 years challenging the bank, and the Law Society’s attempts to remove them from the role (prohibiting them from practising law for life). Both parents were eventually struck from the role.

Dominique Grubisa is currently defending herself against action by the Law Society of NSW which is seeking a disciplinary finding that she is guilty of professional misconduct on 13 grounds, including her claim that her ‘Vestey Trust’ is effective in preventing creditors from obtaining access to the consumer’s’ assets.