See my other posts about Dominique Grubisa.

Update: Claims about Master Wealth Control / Vestey Trust protecting all assets have been found to be misleading by the Federal Court (April 2024). Statements about a court decisions (Sharrment) supporting these claims have also been found to be misleading.

Dominique Grubisa and her companies offer a range of courses and products, including a course on finding ‘below market value’ properties and negotiating deals with distressed sellers (which I write about here), a renovations course, debt management, legal services, loans, insurance – and her Master Wealth Control (MWC) product which purportedly protects your wealth from governments, bankruptcy, banks, individuals and creditors.

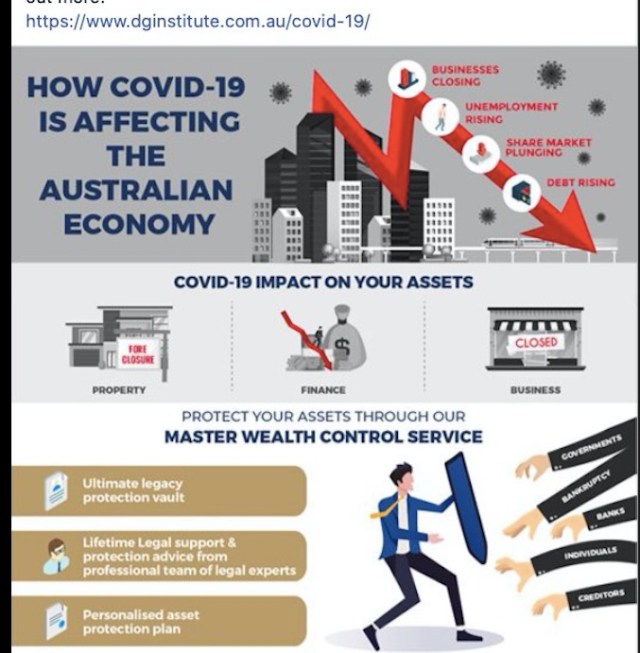

This MWC product (costing about $10,000) has ‘found its moment’ during the COVID19 pandemic. Unlike some other DG Institute (DGI) products, it doesn’t rely on live seminars, and COVID provides just the right environment to increase people’s anxiety and sell a solution.

Building Anxiety

“The COVID-19 crisis will continue to decimate the economy, what are you doing to protect yourself?” asks Grubisa on Facebook.

Grubisa has been warning us to protect our wealth with her MWC for years, and she provides constant messaging about the entities who might seize your wealth. Not just creditors and bankruptcy trustees, but government and banks. In one video she says “the Government can seize wealth – they can do whatever’s required – they can have a bank bail-in. In other words, if banks fail the bank just keeps the depositors’ money – and all of that now, is fair game with what’s happening.”

Grubisa refers routinely to ‘bail-in’ laws. The idea that recent Australian laws allow banks to seize our savings appears to be a conspiracy theory pushed mainly by marginal groups, including One Nation, the Citizens Electoral Council and some people who benefit if we buy gold bullion. Treasury says this isn’t the case, and there are very few main-stream finance experts who support this view. The existence of a conspiracy theory doesn’t prove there’s no actual conspiracy, however if Grubisa’s webinars and “huddles” are all you rely on for your financial and legal information it’s no surprise you may be frightened enough to pay for her ‘protection’

And what about your superannuation? Grubisa says “… governments…may legislate in the future to mandatorily acquire your superannuation.” She says that money in an industry superannuation fund may be more vulnerable than an SMSF if “government changed the law to allow it to draw money held by such institutions” and warns “should the Government decide to pirate superannuation benefits in future….”. This is very scary stuff!

What is MWC?

MWC appears to involve the establishment of a trust which then registers a caveat against real property and registers an interest in other property on the personal properties securities register. The caveat is apparently registered to protect an equitable mortgage and a promissory note from the individual to the trust. The trust can even protect your superannuation according to Grubisa, who says “By this mechanism the equity you have in your fund could be charged with debt leaving you and your trustee in charge of decisions that need to be made.”

The cost of MWC is around $10,200 (“$9,000 for action takers”), which includes “access to Mastermind legal support team for life” and “a personal protection plan”. According to Grubisa the value of the package is $35,000. The DGI website explains “Relying on the so-called ‘man-of-straw’ strategy famously employed by Britain’s Vestey family, it provides an iron-clad vault to protect assets, be they held as property, shares or in other forms”.

Grubisa uses the term “Vestey Trust”. She applied to use the trademark “Vestey Trust”. Grubisa draws parallels with the historic Vestey Trust (established in the late 1800s to avoid paying tax) by saying it became known as “the impenetrable Vestey Trust” and that it survived many legal challenges by the Government. The Vestey companies are probably best known in Australia for underpaying Aboriginal stockmen, causing a famous strike and ultimately one of the early land-rights outcomes.

Grubisa claims “You become bullet-proof, a man of straw” and “you can never fail”. “My law firm has developed a Master Wealth Control Asset Protection system which has been tested and stood up in the Federal Court of Australia”. Grubisa refers to Sharrment Pty Ltd vs The Official Trustee in Bankruptcy. Grubisa says the court said “a trust is a trust”. I’m not sure that the court did say that. As many cases are, this case appears to be based, in part, on the facts of the individual case and whether the bankruptcy trustee could prove the reasons behind the transactions. I’m not sure that the case has much relevance to the legal position of an individual who uses MWC.

Despite marketing MWC as “bulletproof” and “impenetrable”, Grubisa says more about the system in her Kindle book “Real Estate Rescue”. In this book she says of MWC “No asset protection system can spruik itself as impenetrable. Having said that, what we are trying to do is make it difficult for creditors to get to you. The more they have to prove, the more expensive it becomes and the more difficult the exercise. They effectively give up when it comes to throwing good money after bad”.

Grubisa is possibly right about small creditors – who wants to challenge your trust in court over a $5,000 car accident? However, if your unsecured debts are significant, a bankruptcy trustee or the ATO (if you have a large tax debt) may well decide it is worth challenging. Sure ,it will cost them money, but that means if you lose – or even if you get ‘cold feet’ and want ‘out’ of legal proceedings – you’ll probably be liable for the legal costs of the other side. The ATO, in particular, is often a significant creditor when small-business people get into strife and they can be persistent. They may not simply walk away because they see a trust has a caveat over your property.

Is MWC a legal service provided by a legal practice?

While Grubisa says “no”, some consumers may be confused. As Grubisa says in selling MWC:

“…as you know, with lawyers we have professional indemnity insurance – so if I say I’ve got your back – if I say you’ll never ever lose, and this is rock bottom, I have to stand behind that – and the way most lawyers operate, they time charge. If you’ve ever used a lawyer before you’ll know they’re expensive buggers – six-minute units, of billable hours. And what bothered me is, yes I can protect what you have now, today – when that changes, if you don’t come back to me, any of your assets are going to be exposed, and then I haven’t got your back – so you’ll never, ever see this from another lawyer in Australia or in the world but this is underwritten for unlimited changes and amendments for your lifetime.”

“you’re the client. You give me instructions – so what assets you have, what you want protected, how you want the force-field built around what you have. I’m then on your team. I’m your mentor for your wealth control. I set my Mastermind team in action for you – so I am the principal of my law firm which is a national practice – and then we then build the invisible force-field around everything that you own.”

However, if you raise concerns about MWC, you may be surprised to find that Grubisa claims that MWC is not sold by her as a legal service.

As she said to the legal regulator: “Whilst it was made known that the Respondent Solicitor is legally qualified and a solicitor, the MWC Product is not and was not sold as a legal service, nor was it sold by the Respondent Solicitor as such a service”.

Who is Dominique Grubisa?

According to Grubisa, she is a lawyer with a vast range of expertise, experience and contacts in the financial and legal system, who has learned from her own debt crisis and wants to help people by sharing her knowledge. She says she is “also one of the small number of legal practitioners in Australia to have obtained a Master of Laws degree with a specialisation in debt law”. Her mission is “to empower everyday Australians to grow and protect their wealth”.

I assume that to people who don’t have much to do with the legal or financial system, Grubisa’s credentials are impressive.

“More important than what you know though is who you know and for me because of various licenses that I’ve held as a practicing lawyer, as an ASIC credit licensee – I’ve got those licenses that banks have so I know all the judiciary, the legislature, the lawmakers what’s happening – insider knowledge there. I’ve also got a massive competitive advantage in credit markets, banking and finance because I’ve got a money lender’s license too and I know the big guys behind the scenes in the Australian banking landscape”

Who says they “know all the judiciary”? Any experienced lawyer will know some judges, but “all of the judiciary”? …and “the legislature, the law makers”? What does this mean? I’ve never heard anyone say this before. Does she know politicians, or public servants who write legislation? These are strange things to say.

DGI Finance and Master Wealth Control hold ASIC credit licenses – DGI Finance hold a licence to provide credit services (for example arranging loans as a mortgage broker) and Master Wealth Control is a credit provider (ie a lender). There are about 5,000 holders of credit licences in Australia. It seems a long stretch to suggest that she has a licence “that banks have”, or that the credit licence gives her a “massive competitive advantage in credit markets, banking and finance”. And she knows “the big guys behind the scenes in the Australian banking landscape”? What?.

Grubisa also says “I went back and I unpicked all the laws that applied in Australia throughout history, I went back right through British common law and I cracked the code of what the 2% [who are the wealthiest people] do.”

Like a lot of wealth gurus, it is unclear how much of Grubisa’s wealth was made from property investment and development, and how much from selling “education”. I suspect that the skill which has made Grubisa the most money is the one she doesn’t promote – her very sophisticated communications and marketing skills. Grubisa is engaging. Her body language is amazing. Like many gurus she has people who love her and trust her absolutely, and others who feel that they’ve been betrayed. As one ex-student told me, “You’re either with her or against her. You’re either one of the good guys or you’re a bad guy”.

Grubisa’s story about losing everything in the GFC and working her way back from being “homeless” in 2008 is a big selling point.

Within six months of this time she was promoting “Aussie Debt Rescue” on A Current Affair – under the tag “debt busting barrister” and selling her ‘debt rescue’ product through webinars. According to Steven and Corrina Essa who helped her with web marketing “A product that has helped many people and made her a multi-millionaire—just another in the long list of millionaires my Webinar Facilitation system has helped to create.”

By 2013 Stuart Zadel was promoting her presentation “How to make your fortune buying distressed property up to 40% below value…”. In 2015 the Financial Review reported that she established a property scheme in Singapore to help foreign buyers flout foreign investment rules to purchase Australian property.

DG Institute

A number of businesses come under the DG Institute banner, including:

· Master Wealth Control ABN 12 148 036 677

· DGI Wealth Management 65 626 596 272

· DG Institute Pty Ltd 93 618 043 511

· Dominique Grubisa 41 932 057 101

· DGI Lawyers ABN 89 620 718 550

· DGI Finance 33 621 059 756

· DGI Accounting Pty Ltd 50 625 320 363

· DGI Asset Management 45 631 156 897

It can be very convenient to obtain all of your financial and legal services from one place. However, some of the concerns and warnings about property investment one-stop-shops probably apply here, in that all the advice about a particular transaction or product all come from related sources.

However, another risk is that when receiving services under ‘one roof’ clients can be confused about who is providing the product or advice. This doesn’t mean that the business is misleading customers, but people can be confused. Many products and courses involve legal issues, accounting issues, credit issues and financial (investment) issues. MWC may involve all of those, so it’s important to understand when you’re receiving advice from, for example, a licensed financial planner or a lawyer in the course of their legal practice.

Written terms and conditions appear clear, however Grubisa’s engaging presentations are likely to receive more attention from her customers than the written agreement. For example, the terms and conditions on the website say, “By entering into this agreement the Customer acknowledges reliance upon personal choices and decisions and not on any influence, persuasion, warranty or representation made by the Company” and “There are no warranties, representations, covenants or agreements, express or implied, between the parties except those expressly set forth in this agreement.”

According to the DGI website “This legal practice conducted by Dominique Grubisa and her legal services are independent of and not provided by or affiliated with Dominique Grubisa’s other businesses.”

Who are the consumers?

Marketing appears to target people who want to do better financially – and I suspect a large proportion of ‘mums and dads’. It appears that some of the people who pay for the MWC don’t own real property, or if they do, don’t have significant assets. However, she promotes the dream that they will one day – if only they pay for her products and listen to her advice.

Grubisa talks about sharing the “secrets of the top two percent wealthiest people on the planet” and says that these individuals stay that way thanks to their broad networks, smart investments and expert knowledge. She invites readers to “stop and think about how moving into that group…might change your life each day”. Grubisa says:

Positive Thinking

Grubisa talks a lot about staying positive, learning from mistakes, goal setting and sticking at one thing until you’re successful. She says “Commit like your life depends on it” and “stop playing the blame game” as she promotes courses on decision making, mental toughness and negotiating. These are not bad ideals in themselves, but when you’ve spent a lot of money and time on wealth seminars and products, it could encourage you to stick with something that just isn’t a good idea for you. I mean who wants to sound like someone who gives up, or who blames others for their problems?

Pingback: Dominique Grubisa offers 'protecction' amid scathing criticism - World News From Politics

Did she ever or will she ever pay anyone who bought the MWC product

I doubt she’s paid anyone, but she’s bankrupt now. The Court actually ordered the company to pay $15 million in refunds, but that didn’t have much money and it was closed down.

She had the money, she’s hidden her assets.

It’s absolutely criminal!