Lead generation ads on Facebook for financial services can link to scams, or ‘click bait’ promising unrealistic returns that can lead people to switch to risky investments.

Lead generation ads are placed in a bogus business name, often without disclosing the company providing the services, so it’s not possible to know which licensed financial service (if any) is benefiting from the ads.

Even if they don’t lead to a scammer, these ads can result in huge losses, such as when thousands of people lost their superannuation after responding to ‘super comparison’ lead generation ads.

New Facebook advertising rules.

While it won’t solve all the problems, it is positive that Meta (Facebook) has signed on to the Australian Online Scams Code, and has developed a new process for financial services advertising in line with the Code’s commitment to “Deploy measures to protect people from scam advertising.”

From July 2025, Meta requires financial services advertisers to verify the identification of the payer and of the beneficiary of the ad.

So you can still lose money, but at least you’ll know who’s responsible!

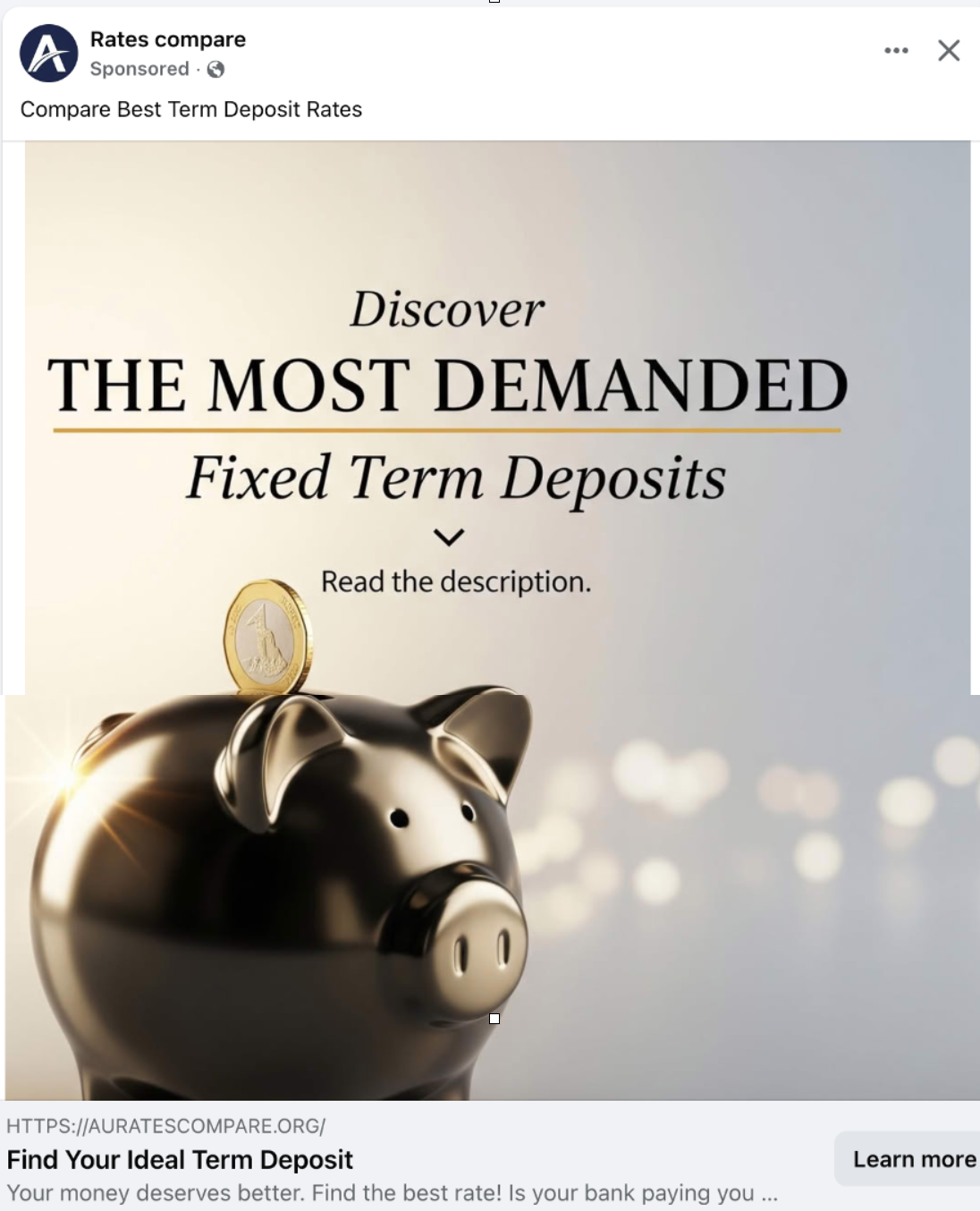

Rates Compare and Capital Guard

While most of the financial services ads I see on Facebook now identify the advertiser, there are exceptions. Like this one, which advertises “term deposits’. The advertiser ‘Rates Compare’ isn’t a real company, and the name of the owner of the website is hidden. My response resulted in a phone call from Capital Guard which holds an AFSL.

The claims by the advertiser, and what Capital Guard offer, are quite different.The ad from “Rates Compare”, claims “Discover the most demanded fixed term deposits”. “Find your ideal term deposit”. “Unlock 9.25% p.a. Returns! Discover the leading APRA-protected Term Deposits”.

The advertiser’s website (auratescompare.org) states among other things “All institutions we work with are APRA regulated and government protected” and “Your deposits are protected up to $250,000 per institution under the FCS”.

However, Capital Guard who subsequently contacted me by phone and email (from Capital Guard’s domain) only mentioned investing in bonds (which are not protected under the FCS). Its website mentions returns up to 7.5% (not 9.25%) and states that “We specialise in the acquisition, custody, and administration of fixed-income securities, primarily bonds…”.

ASIC has warned about “ fixed-income products being advertised as term deposit ‘alternatives’ or ‘substitutes’, and consumers investing significant sums as a result.”

The phone call from Capital Guard is possibly in breach of the anti-hawking provisions, because the consumer is induced to consent to the contact so that the consumer can take up another service (in this case term deposit comparison). See ASIC’s RG 38.68.