The Australian Government is considering how to curb lead generation activity, following over one billion dollars in losses by consumers who were funnelled to unethical advice via lead generation advertising. So what happens if you respond to a “free superannuation review”?

Social media is still full of these lead generation ads, so it’s not difficult to find out.

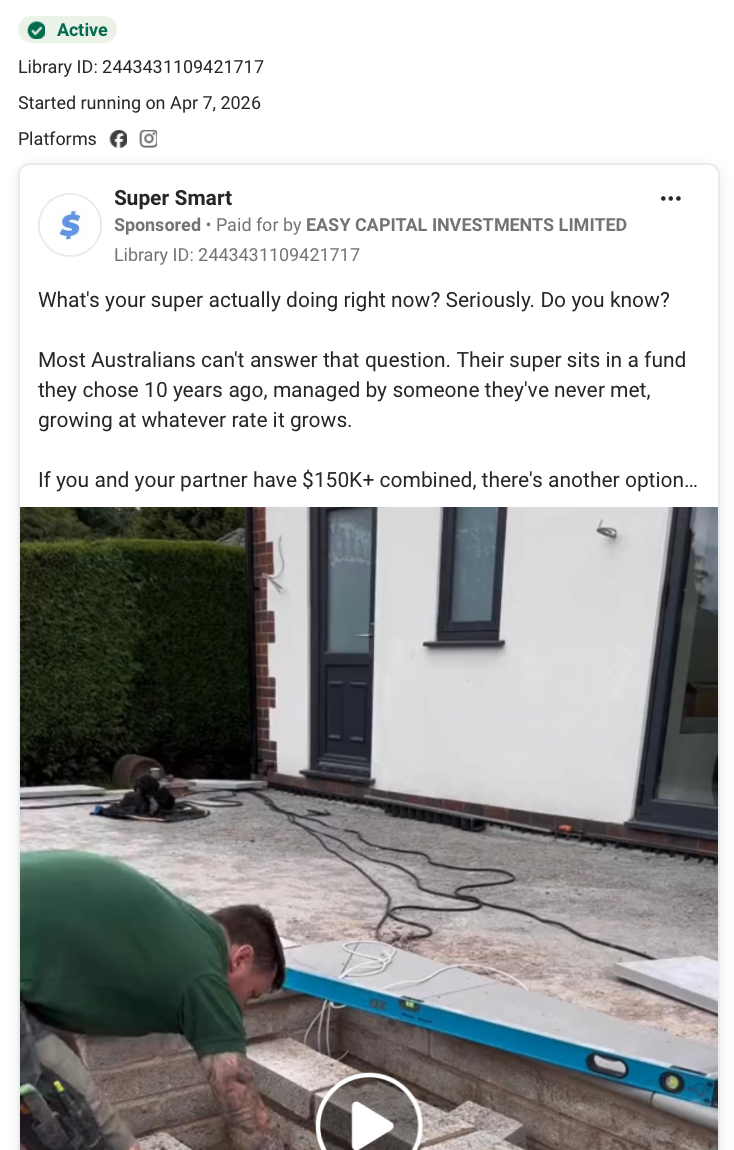

This week I responded to a Facebook ad by “Super Smart”. The video said “review your super performance in just 60 seconds …. just click the link below it’s free.” Other ads by Super Smart promoted property investing through superannuation. These ads suggested there was some urgency, claiming that the law that allows this could change soon.

The ad identified that it is paid for by NZ company Easy Capital Investments. It appears that the director of Easy Capital Investments is also a director of Velocity Leads.

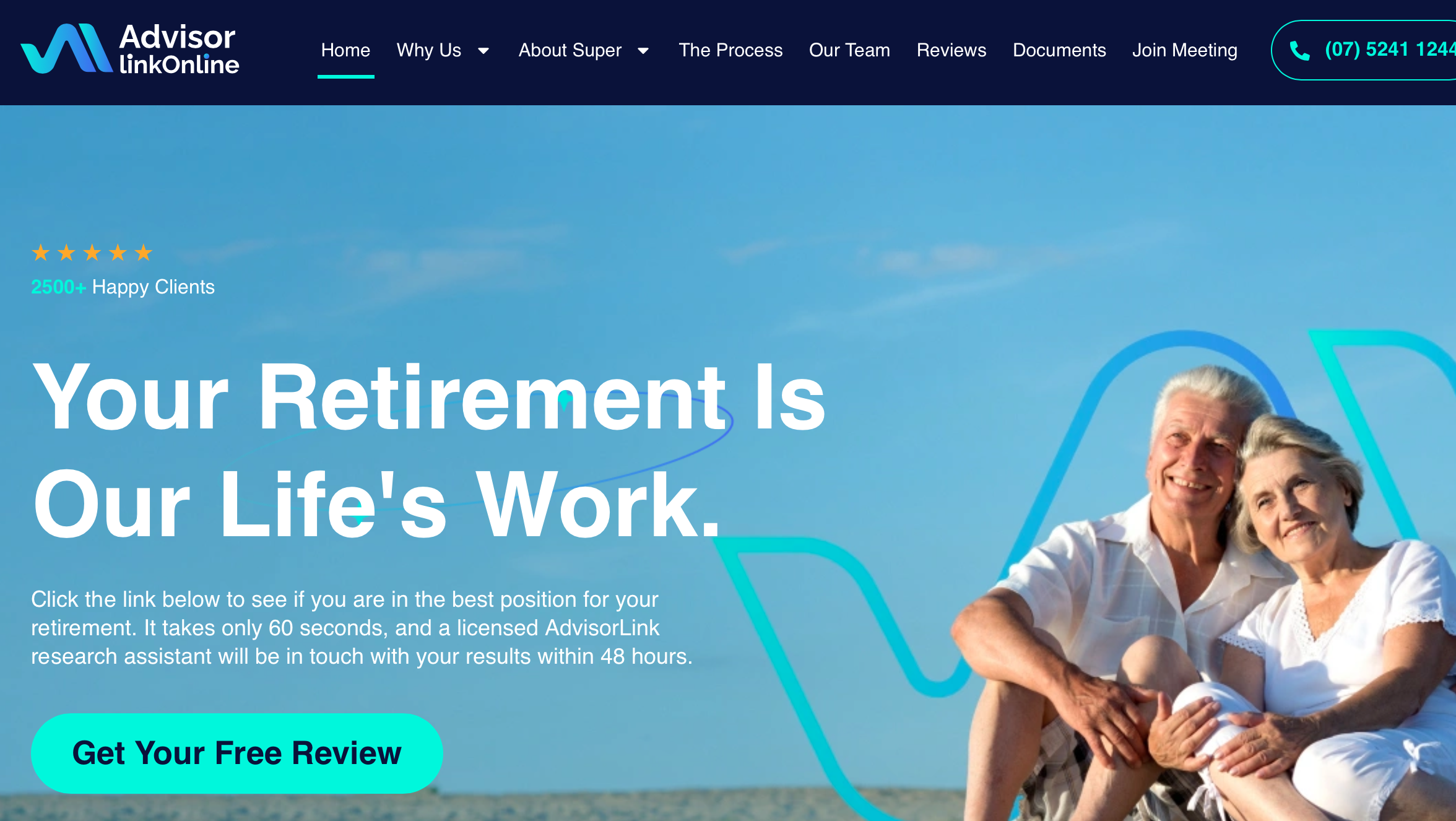

Within minutes I received a text referring to my enquiry, saying to expect contact from Advisor Link.

I received a phone call 5 minutes later from Advisor Link (I think all communication was with Travis Seckold, the director) asking for some information so my free report could be prepared.

In response to his questions I told him I was 65, earned $80,000 a year, and had $500,000 in HESTA superannuation and my funds were in Hesta’s default investment option. (This information, and the name I provided, are fictitious). I received an email 5 minutes later saying that my report was being prepared. This email said “On average we see a projected increase of $300,000+”. Two hours later I received a text saying that my “Free Superannuation Health Report” was completed, but it said they needed to call me because “There are a few concerns that we would like to make you aware of”.

I suspect it is part of the process to make this second phone call before providing the report – there was not much information in this call apart from an attempt to try to move me to a financial advisor. Travis used this call to point out that being 65 it was important I was in a top performing fund – that they have to put me in a better fund compared to my current fund. He said “it has to put you in a better fund compared with 6.99%”. He said he could show me if I was near my computer – I think he wanted to do a video call but I declined this. .

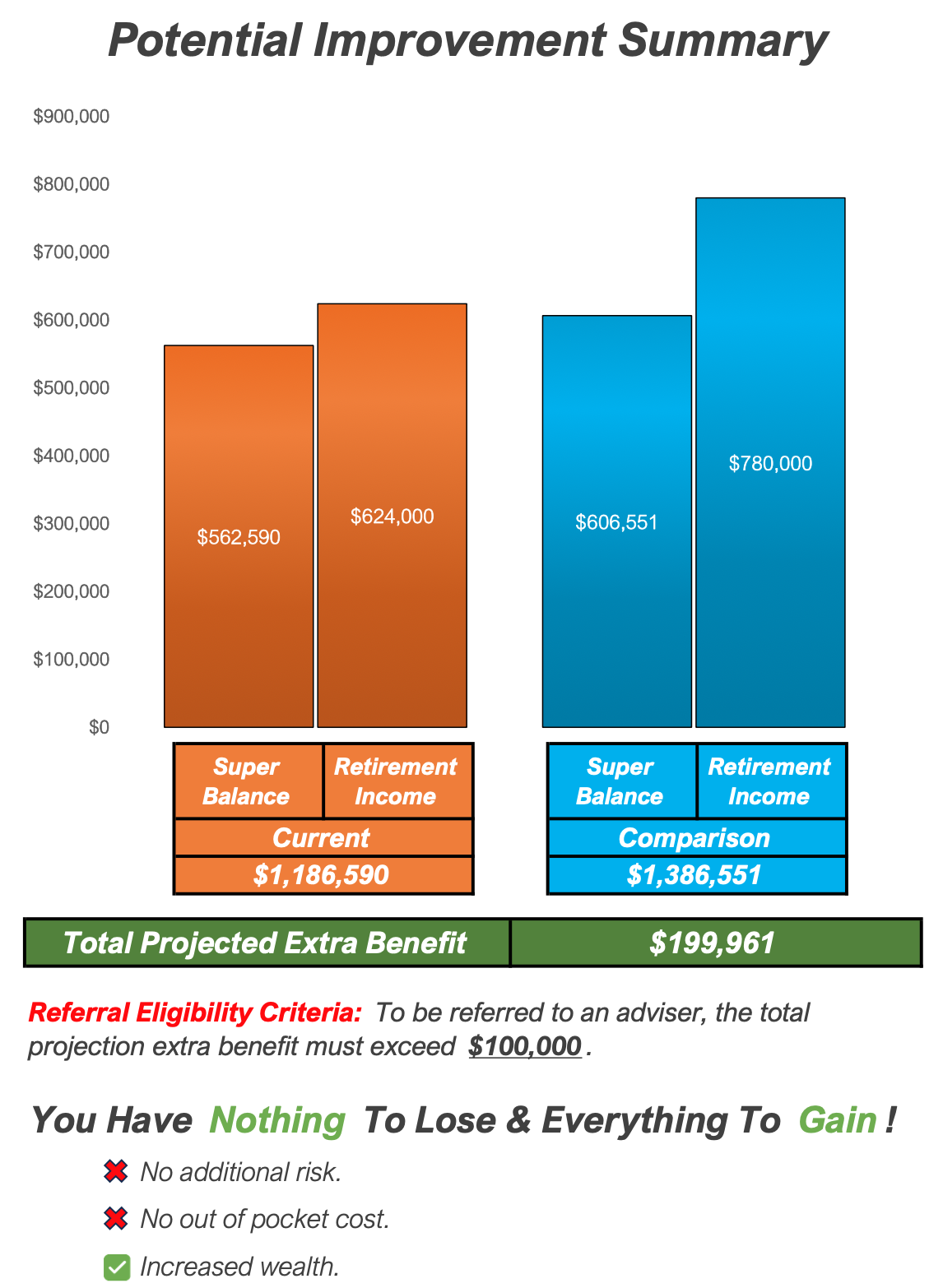

He said with my current fund I could take $54,000 per annum income once retired in two years (at 67), which would run out at 79. He told me the comparison would give me an extra benefit of $199,000. He said this is “not financial advice. It’s like going to a doctor before you have surgery”. “The Government says any advice relating to superannuation, is paid from your super. All our advisors are checked and licensed”.

He said “To be referred to an advisor, the benefit must be at least 100K or it’s illegal”! “You’ll only be shown personal advice if it’s in your best interest.” He mentioned something about not putting me into any of “those high risk products”.

Hs said he can refer me to Stefano Duro. “He’s one of the best in Australia. He’s a judge at the national financial awards. Do some research on him.” “He’s the surgeon, this is like going to the doctor before you have surgery” (yes he said that again!). “I’ll book you in with Stefano now”. I declined, but I did do some research. Despite a very sleek website, the fact that Duro mentions Grant Cardone and Gary Vaynerchuck (pictured below) in his profile would be enough to put me off!!

The process was very slick – I assume the intention is to move the customer quickly, and seamlessly, from ad, to phone call, to email to financial advisor.

So what was in the Superannuation Health Report? It started with a screen shot of the ASIC registration of the Advisor Link company. The “selected, vetted referral partners” are listed – Inheritance Financial Advice, My Advice Hub and Pure.

The report contained the personal information I’d provided, and assumed I would retire in 2 years time, aged 67.

The new super fund’s 5 year return after fees was 11.79% (compared to my current fund 6.99%). The report explained that with the new product my super balance in 3 years would be about $44,000 more, and the retirement income would be about $156,000 more. These are added together to give a “total projected extra benefit” of almost $200,000. This results from some double counting because they add the super balance to the retirement income, which already includes using up the super balance (see below).

The comparison fund isn’t named. While the report says the “investment risk strategy” of the comparison fund “would be matched with existing super fund”, the category assigned by Advisor Link – “growth” – could cover a wide range of investment options, with different risk profiles. An 11.79% return with a similar risk profile to my current fund seems grossly unrealistic.

There are a number of problems with lead generation in the financial sector, including the ability of unlicensed companies and individuals to influence someone’s investment decisions before they receive licensed financial advice. Even if the licensed advisor acts ethically, a report that shows such a large financial return could lead someone to expect the advisor to achieve that return. Even if the advisor explains that there is increased risk, would a person be conditioned to expect that return more readily and accept a higher risk that they might not have otherwise?

The risk for the consumer is that they don’t simply obtain a comparison between super funds from the lead generator. They receive a report that projects their financial future based on a particular (but unnamed) superannuation fund and investment strategy. By the time they see the advisor, they may feel they have already received some advice, and may feel they know their best superannuation option. While technically separated from the subsequent provision of licensed financial advice, in reality I doubt most consumers could completely separate it in their minds. How does the financial advisor deal with a consumer who has received an overly optimistic projection? Can you imagine the advisor saying “Now, please forget what these marketing people told you, the investment they proposed is likely to be inappropriate”.

Licensed advisors who pay for these referrals are compromised. The conflict is a real one – do you place the client in the fund that’s proposed by the lead generator even if it’s inappropriate, or do you lower the client’s expectations? How do you act ethically and keep the referrals rolling in?