Should life insurers benefit from dodgy advertising under fictitious names?

With the potential for a ban on lead generation for financial services, the life insurance industry body, the Council of Australian Life Insurers (CALI) argues for life insurers to be exempted. (see IFA News 10/6/26). Admittedly, the risks for consumers are not as great as they are for superannuation and investments, and there is arguably a place for allowing life insurers to receive consumer enquiries through legitimate comparison sites. However, that is not the only example of lead gen for life insurance.

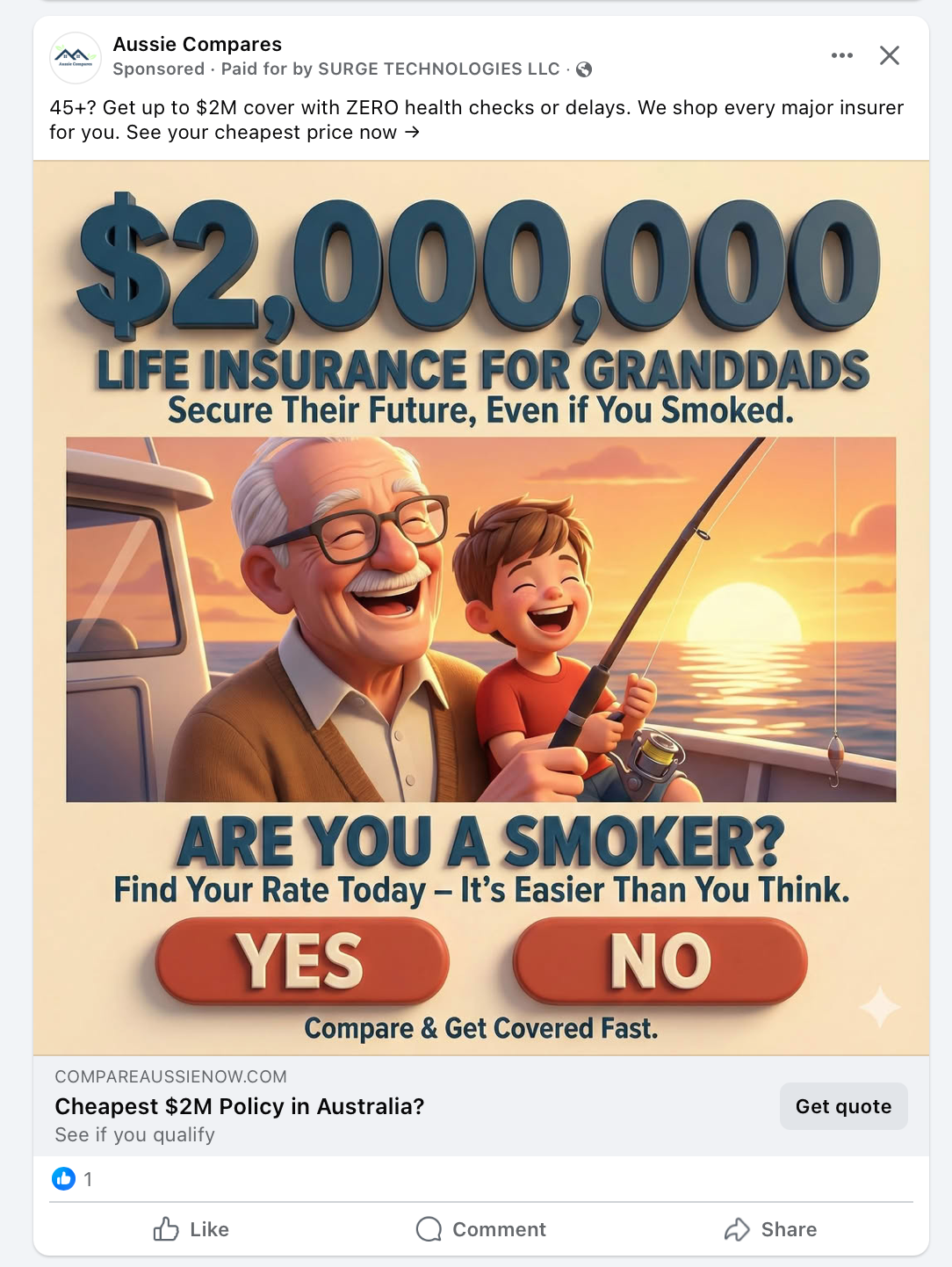

Social media is full of life insurance advertising under fictitious names, which don’t identify the licensee that benefits from the ad, and often make misleading or exaggerated claims (in some cases a license number is provided, but it appears to be incorrect). From my experience (responding to these ads), they tend to result in calls from large comparison services (insurance agents) such as Compare Club and SaveU, but you won’t know until you share your details and get a call. These services are “licensed representatives” which are entitled to represent a financial services licensee – so why are these services reluctant to identify their name in these ads?

Insurance agents and life insurers publish ads in their own name, but these are more restrained than the anonymous lead gen ads. It appears that hiding the name of the licensee encourages dodgy advertising.

Examples of the lead generation advertising include:

- Offering “compare multiple insurers in just 60 seconds” when you are required to provide some personal details and wait for a telephone call

- Highlighting “no two-year waiting period”, where most life insurance don’t have such a waiting period

- Targeting older people and “leaving a legacy” for grand children

- Focusing on pre-existing conditions

- Including age groups for a potential quote (for example 79-85) where it appears that the relevant comparison service excludes this age group if you try to contact through its website

- Case studies that appear to confuse death benefits with income protection

It’s unlikely that the life insurer is aware of the content of these anonymous ads, and the comparison services that pay for them are also probably disinterested.

However, many of the consumers who respond to these ads are ultimately customers of a life insurer.

These ads don’t paint the industry in a positive light, and insurers should support banning life insurance ads that don’t identify the licensee.